Credit Information Bureau India Limited (CIBIL) calculates your CIBIL Score, something that is based on current financial analysis and other monetary references (CIBIL). This is a three-digit number ranging from 300 to 900. The stronger the credit (CIBIL) number, the more financially healthy you are, and the more certain you may be to become authorized for a loan, along with a personal loan at a reduced interest income.

The credit companies in the country generate credit scores based on a variety of characteristics such as the duration of your credit record, payback histories, and credit queries, among many others. When applying for a credit card or a loan from a banks or an NBFC, having a better credit score may qualify you for additional perks such as a lower interest rate and a longer repayment period.

Why is CIBIL Score Important?

Throughout the loan document verification, the CIBIL Score is quite important. When a potential applicant finalizes and undertakes an approval process for a loan, the creditor verifies the CIBIL score as well as the bank’s data. When a score is low, the creditor could refuse to examine the credit online form for subsequent clearance. Banks and different financial companies use this value to determine if you qualify for a credit facility, a mortgage loan, and other such consumer credit.

Because private loans are uninsured, they don’t necessitate a lot of paperwork. It doesn’t also encompass the use of mortgages or assets as a form of collateral. Nevertheless, the lender or bank or financial firm will assess your creditworthiness and competence to cover both the principal and interest constituent of the loan. Along with standard essential qualifying conditions, the candidate’s creditworthiness is evaluated during this stage through the use of the Credit Information Bureau (India) Ltd. credit summary score.

Factors Affecting Credit Score:

Positive Factors:

- Timely Payment of credit card dues

- Payment of loan EMI on time

- Payment of not only minimum current due but the entire amount before time.

Negative Factors:

- Possessing too many credit lines especially in the form of unsecured loans

- Non- payment or late payment of bills on credit card or loan EMIs

- Consistent use of credit card limit up to 75%

How much credit Score should you have for Personal loans?

To maximize your prospects of acquiring a higher loan and having it approved, you can aim for a credit rating of around 900. The significant proportion of creditors acknowledge a credit score of 750 or higher to be optimum for credit facilities. As a result, you may conveniently avail a bank loan beyond this value. If your credit score is around 800-900, you can acquire a loan at a substantially cheaper rate of interest than the industry average. According to research released by the Economic Times, if the credit score is greater than 750, 80 percent of loans are granted.

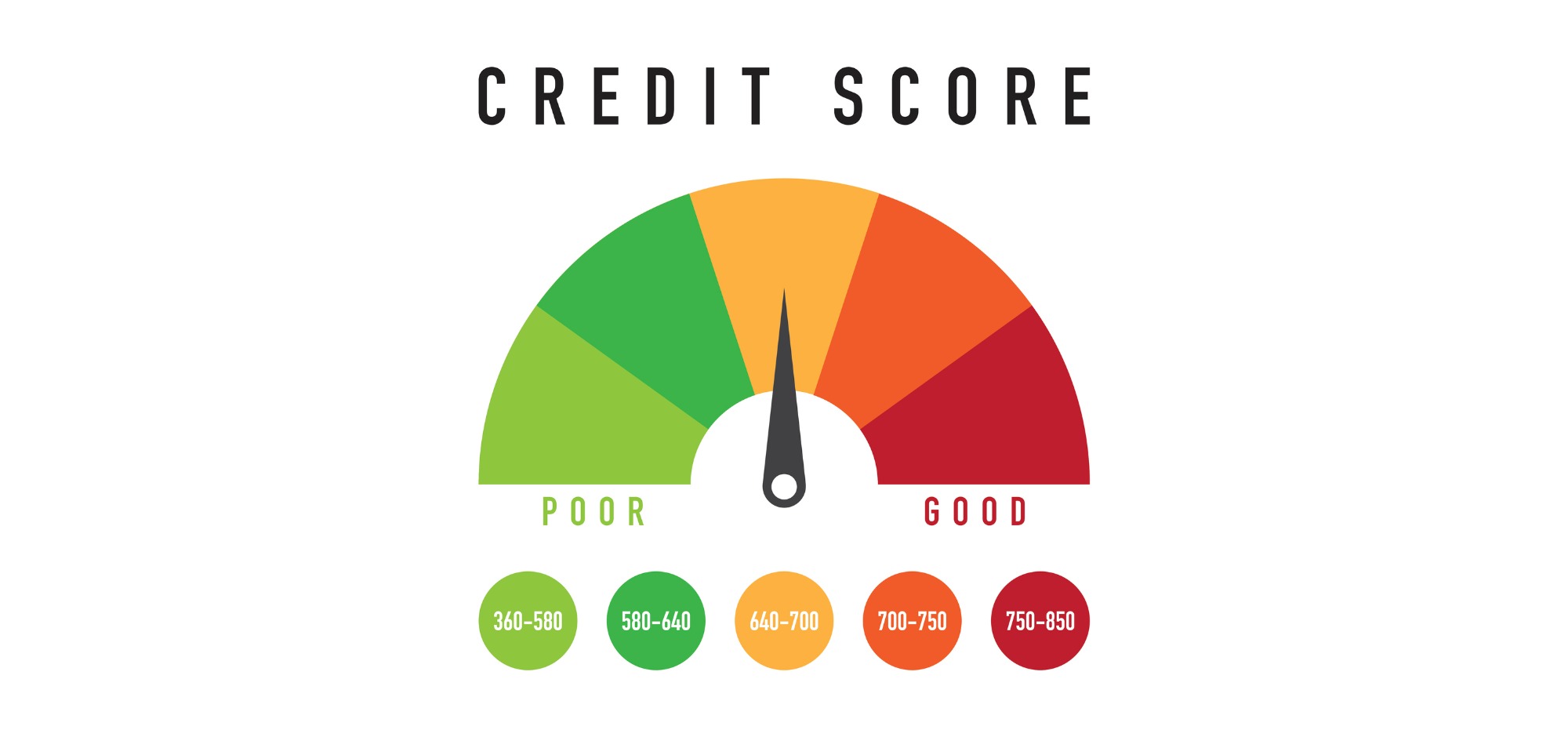

Credit Score Range:

NA or NH:

This emphasizes that individuals possess no credit record. This could be because you haven’t collected out a loan or utilized a credit card so far.

Credit Score Range of 350 to 549:

A CIBIL rating within that band emphasizes that you have a poor credit rating. This indicates whether you have been liable to repay your credit card payments or bank EMIs. You therefore possess a larger risk of deferring on a personal loan, making it harder for you to obtain one

Credit Score Range of 550 to 649:

The CIBIL Score should be in the range of 550 to 649. Even so, not every creditor will accept you for a personal loan based on your credit score. To give a loan at about this personal credit band, several institutions demand an increased percentage of interest.

Credit Score Range of650 to 749:

Credit scores in the range of 650 to 749 are ideal for loan banking institutions and financial organizations. There’s a strong possibility you’ll acquire a personal loan, but the rates in this band may not always be the optimum.

Credit Score Range of 750 to 900:

It is the optimal and desirable range, so you’ll have a good chance of getting the greatest prices from top-rated banks or NBFCs.

The Best 5 Solutions to Increase Your Credit Score:

As an applicant, you may make a sensible and timely commitment to repaying your debts, which can help you build your creditworthiness in the coming years. The following are the top five steps to achieving this:

- When you register, evaluate your credit score: Users can monitor their credit reports immediately and spontaneously on CIBIL’s official site, and you should generally review your result before submitting an application for a loan or credit card. You will receive it online or by courier for Rs. 470. It benefits in two aspects: you can be assured that your credit score is free of potential drawbacks and apply with confidence, and creditors can identify which other lending institutions have denied your request, so don’t move forward if your score is low.

- Make on-time credit card deposits: Failure to make on-time credit cards or repayments might have a detrimental impact on overall credit ratings.

- Build a credit record if you don’t have one: Many first time borrowers might not have had a credit record on which banks can base their decisions. Their credit rating is zero or negative, which is why banks and other financial organizations may be hesitant to lend to some of them. They can, however, deal with this obstacle by maintaining a fixed deposit and using that to secure a credit card. They can increase their credit record by making frequent transactions on this credit card.

- Split your spending over different credit reach: Your credit report may suffer if you have numerous credit cards but still use only one to make large purchases. Spreading your expenses across numerous credit cards is preferable to deciding to put a considerably higher amount on a single card.

Important Credit Score FAQs

- 1. What exactly is CIBIL?

The Credit Information Bureau of India Limited (CIBIL), which was established in 2000, keeps track of a person’s credit cards and loans. The ISO 27001:2005-certified CIBIL is split into two branches: consumer bureau and commercial bureau. The consumer bureau, which began operations in 2004, has almost 260 million records, whereas the commercial bureau, which began operations in 2006, has around 12 million records. CIBIL’s technological collaborators are TransUnion International and Dun & Bradstreet. - 2. How do you find out what your CIBIL score is?

To receive a specific credit score, go to the CIBIL portal and select the ‘know your score’ option. Complete out the online form that asks for information like your name, birth date, earnings, proof of identity, address, and contact information, as well as the loans you’ve signed for. You will be required to enter identification information that comprise inquiries regarding credit record, after completing a particular amount of transaction. Your credit rating will be provided to you after validation. - 3. Who determines a credit score?

When you complete a payment that is important to your credit rating, your bank sends information to all four credit reporting agencies. The RBI has mandated that records be sent to all credit reporting agencies. In essence, banks hold Credit Information Companies regularly updated on your financial activities. If a bank wants to test its creditworthiness instantly, they can go to any of the bureaus online and all four are equally authoritative and comparable.Creditbureaus begin obtaining additional details regarding your monetary activities from other financial institutions organizations after getting data from the lender.

Credit reporting agencies begin obtaining additional details regarding your finance activities from other banking and other financial organizations upon obtaining reports from the lending institution. The credit companies then use this data to create what is known as a credit score. - 4. Why do I need to know my credit score?

It is critical that you monitor your credit rating closely. This is the most accurate approach to assess your prospects of obtaining a line of credit. A further purpose to keep monitoring of your credit report is to see whether it drops or if credit bureaus make a mistake when generating it. You will be able to undertake quick and effective corrections as a result of this. - 5. Can monitoring your record have an unfavorable impact on your rating?

Once every year, analysts recommend verifying one’s CIBIL rating. The procedure is referred as a soft inquiry,’ in contrast to credit card companies requesting your score from CIBIL, which is described as a ‘hard inquiry.’ Furthermore, applying for a loan with multiple banking institutions around the same period could lead to hard inquiries, which could lower your credit score. - 6. Will using a credit card lower my credit score?

There’s no need to be concerned if you maintain zero interest payments or debts on your previous credit card. If you’ve had a credit card with a good creditworthiness, it will represent overall appropriate financial activity while also lowering your utilization rate.

{kind=link}